We are researching Opyn protocols: Squeeth, Gamma, Convexity. Integrated with Ribbon, StakeDAO, PODS, and Olive (formerly Polysynth).

Let’s double check if each launch candidate is valid by our strict criteria: on chain, open source, and easy dependencies:

On Chain: All operations should be smart contracts should be written in Solidity, executed on chain in Ethereum Virtual Machine (EVM), and immutable after secure settlements – except minimally-scoped governance (parameter changes or contract upgrades) and well-defined liquidation (over margins or strike conditions).

Open Source: All code should be public source with open development of reviews and commits, readily forkable and re-deployed to any compatible chains; hence, code snippets, partial features, audit snapshots, or missing frontends are insufficient.

Easy Dependencies: All components should be checked against vendor lockins and security risks; in particular, the use of ChainLink must be compatible with Band (Harmony’s oracle) and Uniswap V3 fork is our only spot market. Also, the pull oracle Pyth, the custom oracle Redstone, money markets, staking networks, market makers, off-the-counter services will not be available in coming months.

We focus only on derivatives as they drive active trading without large token ecosystem or high collaterial requirements. Therefore, we will skip stablecoins, lending, aggregators, sport gamblings, and prediction markets – until more traders have bootstrapped.

Two important concepts for squeeth are the funding rate — the interest rate paid from long squeeth holders to short squeeth holders; and implied volatility — the prediction of volatility embedded in the squeeth price.

We use these measures for the same reason we use yields for bonds or implied volatility for options: they can be interpreted directly and compared across time. We are particularly interested in these for squeeth because, under some simplifying assumptions, the funding rate is the variance (the square of volatility)*.

… a pricing formula for a squared exposure to an asset derived under the same assumptions as the Black Scholes Merton option pricing formula [Power futures technical primer – on Google Colab]: Squared ETH future = ETH² * exp(volatility²)

It means that DeFi markets can be unified, and that pricing and liquidity can be significantly better for everyone. It means that fragmentation between protocols is less of a problem than we thought, since the building blocks of defi fit together better. It means DeFi can beat CeFi because our blocks fit together better than their blocks.

Opyn Markets is the perpetual contract version Uniswap. Anyone can deploy a contract trading market on any asset without permission. TradFi margin meets linear, curve, single LP and flexible collateral. The project raised a total of US$8.86 million.

The mathematical intuition is that after removing a the linear component of a function you are left with quadratic and higher order terms. This is why we can quite accurately hedge any non-linear exposure with a linear instrument (futures) and a quadratic instrument (SQUEETH).

Uniswap v3 positions have no gamma outside of the range, so the hedge needs to reduce to zero. Practically this means you need to run wide ranges or rebalance frequently to ensure the SQUEETH gamma has some Uniswap gamma to hedge.

The option delta and gamma can be calculated from the option price given the current ETH price, the strike, and the expiry: [Hedging options with squeeth – on Google Sheet].

In terms of the “real” funding rate, it has been 0.07% per day for Opyn’s Squeeth (see below). This corresponds to APR of 25–26%; however, do note that Squeeth worth just 12.5% of the position’s value must be bought, there for the real second-order funding range is just 3–3.5% APR of the position’s value.

Uniswap positions as options: LPs are most profitable in crab markets, when price is moving sideways, and most risky when large price moves happen. Buying astraddle or a strangle is therefore a way how to insure an LP position — it’s a bet on volatility, with delta-neutral outlook (no need to guess which direction the price will move).

But there’s a deeper connection between LP positions and options. A concentrated liquidity (CL) position’s value function has the same shape as covered call option strategy value, which has the same shape as short put option strategy. Creating Uniswap CL positions <=> writing covered calls <=> writing put options. (“<=>” here means similarity, not equality!)

Squared ETH, also known as Squeeth, is a perpetual options system that allows for unbounded upward leverage and no liquidation of long holdings. Opyn's Research Team (Zubin Koticha, Andrew Leone, Alexis Gauba, Aparna Krishnan), Dave White, and Dan Robinson designed Squeeth (squared ETH), a novel financial derivative. Squeeth is the first Power Perpetual, providing traders with continuous exposure to Ethereum squared.

The Opyn team launched Squeeth on the Ethereum mainnet on the 11th of January. Squeeth (short for squared ETH or ETH2) is a product created by @opyn_ that combines elements of options, leverage, and perpetual swaps while eliminating strikes, expirations, rolling, and liquidations for longs. With the introduction of Squeeth on January 11th, Opyn launched The Crab Strategy on January 14th, a contract that will automate rebalances to preserve delta neutrality, allowing users to deposit ETH and earn yield with minimal upkeep.

According to a Jan. 9, 2022 blog post by Wade Prospere, head of marketing and community at Opyn, the basic purpose of the new tool is to give traders exposure similar to highly leveraged bets they could get from trading options, but without the need to set strike prices or determine contract expiration dates. Squeeth converts the options exchange into a permanent contract that can be utilized as a hedge. The trade gives leverage without liquidations on the long side — speculating on price appreciation.

The ability for Squeeth to hedge against Uniswap V3 LP positions is a monumental development because a recent study by Bancor showed that hyper impermanent loss was responsible for 49.5% of liquidity providers left with negative returns. The only time horizon which managed to avoid significant loss was those flash LP-ing within a single block (Just In time Liquidity, JIT). Therefore the practical implementation of automated hedging strategies for LP positions integrated with active Uniswap V3 liquidity managers could potentially reduce these losses to 1%, if hedged accurately.

Currently, Ribbon’s revenue model is based on withdrawal fees from vaults, which is set at 1% for the protected put USDC and Yearn USDC vaults, and 0.5% for the covered call vaults (ETH, WBTC). While this has generated Ribbon over $600k in fees so far, it makes it expensive for users to move funds into and out of vaults.

Ribbon passed a governance proposal on June 2nd that distributed accrued fees and future V1 fees back to their respective vaults. Notably, Ribbon is switching from a fixed withdrawal fee to a management and performance fee in the future. This will reduce the friction of moving in and out of vaults. For example, if a user believes the market structure is changing from low vol to high vol, they could easily move their capital from the Theta Vaults to the Delta Vaults free of charge.

Do L2 protocols, gas-free offerings, and partial collateralization bring significant volume? Does the set-it-and-forget-it style of structured products continue to dominate the volume or do we see an influx of active trading and hedging? Does Opyn launch a new derivative offering or create a market for one?

Opyn Squeeth (oSQTH) is a new financial primitive that tracks the price of ETH squared. Squeeth works like a power perpetual, using an index price and funding rate to ensure that the contract trades at equilibrium price. Opyn Squeeth is an ERC-20 token, and users can simply buy oSQTH from the Uniswap v3 oSQTH / ETH pool. Users can also mint oSQTH by providing ETH as collateral to Opyn.

Long Squeeth provides exposure to pure convexity, offering an asymmetric payoff with a higher upside and lower downside. As indicated in the chart above, oSQTH makes more when ETH goes up, while it loses less when ETH goes down. However, long Squeeth holders pay a high funding rate to maintain this asymmetric payoff. Therefore, holding Squeeth over extended periods during sideways and bear markets may cause a loss in exposure to ETH squared.

The time that a position has remained open, and its correlation with fee revenue as a proportion of [Impermanent Loss] IL is worth further comment. The only group that we could identify that consistently made money when compared to simply HODLing was flash LPs who only provided liquidity during one block. This behavior has since been coined Just-In-Time (JIT) liquidity. In this group there was no meaningful IL. In the other groups the IL / fees ratio was always >100%, meaning they lost out. In fact, it went as high as almost 180%, meaning a loss of $180 for every $100 earned in fees, leaving a net loss of $80.

JIT liquidity notwithstanding, shorter positions seemed to be more profitable when examining fees earned per unit of time; however, the fees on such short timeframes were overshadowed by their [Impermanent Loss] IL. The shortest-lived positions (of those longer than one hour) generally and consistently had the worst fee-over-IL (akin to risk-adjusted returns) ratios, and the longest positions (over 1 month) had the most forgiving fee-over-IL ratios, although both groups lost money. To explain this effect, we refer to our earlier economic analyses of the AMM model, and specifically the fact that IL grows in square root time while fees accumulate linearly in time.

Olive has closed a $3M Strategic Roundfrom strategic partners — LedgerPrime, QCP Capital, Morningstar Ventures, LUX Capital, CSP DAO, Key Opinion Leaders, and Community Oriented DAOs, along with active participation from our existing investors. We are also highly grateful for the continued support from Sandeep Nailwal, Jaynti Kanani, Brevan Howard, Jump Capital, Hashed, DeFi Alliance, Smape and others.

There is a lot of potential for creativity and composability in the future. Vovo has other yield-enhancement products that incorporate [GMX LP Token] GLP, and is working on additional vaults that integrate with Primitive Finance and Squeeth. Brahma has principal-protected vaults that accumulate risk assets such as MATIC and ETH. Ribbon has announced plans to develop a similar vault for ETH and BTC.

01: Another (surprise) derivatives exchange offering both standard perps and power perpetuals, a product similar to Opyn’s Squeeth. These are like regular perpetuals but raised to a power, offering option-like exposure. They use Pyth for their funding rates.

Opyn’s growth in TVL was an outlier to other options protocols. This can be attributed to their new product SQUEETH, a financial primitive we recently covered in a post here. Trading volume of SQUEETH has risen steadily over the past month, but its take-up rate hasn’t been outstanding. This may be due to the complexity of understanding and trading such a product.

Long Squeeth provides exposure to pure convexity, offering an asymmetric payoff with a higher upside and lower downside. As indicated in the chart above, oSQTH makes more when ETH goes up, while it loses less when ETH goes down.

Capital inefficiency remains a major problem in the options space due to the full collateralization of options. Traditional market makers can use a variety of hedging instruments to limit the capital burden of their liabilities. While order book protocols like Opyn and Zeta already employ partial collateralization and cross margining to boost capital efficiency, such mechanisms are more difficult to implement for an AMM. Therefore, notional open interest is capped by value locked in the protocol.

As mentioned earlier, most attempts at decentralized asset exchanges have been rather focused on either spot or one type of derivative. dYdX, MCDEX, Perpetual Protocol, Futureswap, Drift, and several others support perpetual futures (and perhaps expirable futures eventually). Opyn, Hegic, Dopex, Lyra, Primitive, Psyoptions, and others are building on-chain options products.

Options and Structured Products: While perps are a massive market within crypto, we are arguably more excited about the burgeoning options space as we look forward to 2022. Ribbon and Opyn kicked off the first decentralized options products that actually made sense back in April. Since then, we have seen the rise of various L1s and L2s that have made option protocols within DeFi more feasible.

Two options projects we are excited about: Zeta Markets: “Building the best in class decentralized options exchange. Base infra is Serum orderbooks with a native Zeta AMM plugged into it. With an AMM, Zeta will overcome bootstrapping issues with decentralized options OBs like Opyn. And via the orderbook, they’ll be able to overcome UX barriers presented by options AMMs. Coupled with high throughput, low latency, low fee environment of Solana, this could be THE options project that is able to incentivize institutional players to seriously trade options in DeFi. Also, the first team to recognize the importance of expirable futures in the hedging process for dealers. Did I mention the AMM will eventually delta hedge for casual LPs?” – Ashwath (Twitter @Ashwathbk)

Demand for Ribbon options continues to rise, as evidenced by its TVL growth as the DPI (a DeFi index) fell hard. Ribbon uses Opyn as its settlement layer, and demand has been so strong that Ribbon now represents over 85% of Opyn’s TVL. At times, Ribbon’s TVL has even exceeded Opyn’s — which is explained by the time differential in users depositing assets to Ribbon and Ribbon vaults deploying those assets.

Ribbon is partnering with large options market makers to source liquidity for all of the new products they launch. These market makers will be the counterparty to all Ribbon vaults, taking the opposite position of the vault. For example, Ribbon’s next product is a vault where LPs can deposit ETH and the vault sells covered calls against it. Ribbon wouldn’t sell calls on Opyn or Hegic, but would instead sell it to these market makers who can then go and hedge their exposure on Deribit. As the DeFi options market evolves, Ribbon will pivot from using off-chain market makers to on-chain options.

Ribbon’s strangle taps into Hegic for liquidity, but there’s one problem there: DeFi options protocols cannot service a lot of demand yet. Liquidity provision models for popular DeFi options protocols are bit tricky. Hegic LPs hardly break even and rely on HEGIC emissions to actually make money. Opyn options are now just limit orders on 0x, and the orderbook is illiquid even around the few durations and strikes Opyn has. We have protocols like Charm Finance that have built options issuing infrastructure that is capital efficient and priced at par with the market. But Charm is still in the process of developing tools to make the UX for LPs much better. Overall, the DeFi options vertical is nascent and yet to develop the kind of liquidity DeFi spot markets see.

Keeper Bot in action: The KeeperDAO flash loan pool was used for the recent Opyn exploit. A DeFi trader integrated with KeeperDAO to flash borrow and exploit Opyn’s contracts via Uniswap.

On April 23rd, Hegic announced the V1 launch of its protocol, which allows users to buy or sell American put/call options on Ethereum. We first wrote about Hegic on March 20th in our Thematic Report on Insurance Products. In that report, we also highlighted Opyn, a similar on-chain options protocol. What differentiates Hegic though, is how it writes (sells) options by implementing liquidity pools.

Thales positional markets have performed poorly. This is explained by growing pains as Thales perfects its pricing mechanism for binary options without the luxury of Chainlink feeds for implied volatility. Early on, Thales had artificially high values for [Implied Volatility] IV while the market settled calmly. This allowed users of the popular “crab” strategy to sell optionality for a high price. For ETH and BTC, IV is pulled from Deribit. Other assets’ IV values are derived from historical volatility against ETH. The performance of the options AMM should improve over time. Most options AMMs struggle with mispriced IV early on.

Convexity: The age of collateralizing derivatives positions with the native asset is coming to an end as traders rapidly shift from coin-margin to cash-margin (stablecoins). We glossed over this in a previous daily, and the effects of this are profound. For starters, shorts lose their innate hedging and positional convexity.

When BTC price goes up, shorts with BTC as collateral have a natural hedge because their margin (spot BTC) goes up. With stable-margin, shorts are naked as they don’t own the BTC they are shorting. Longs on the other hand are exposed to less downside risk when BTC goes down, because they don’t get hit with the double whammy of their derivative position and spot margin going losing value in tandem.

Crypto Margined Futures Continue Trending Downwards: Since May 2021, crypto-margined futures have been on a multi-month downtrend as cash-margined futures gain a significant share of futures [Open Interests] OI. One of the main implications of this is reduced directional convexity.

Arguments: The 5% fee charged by Fei Protocol would only cost Synapse $625k per year for comparable levels of liquidity being purchased with 4.5m SYN. Additionally, as the protocol has the variable tranche of the pool, Synapse would earn yield from the pool’s trading fees. Fei Protocol has also allocated $1.4m USD in TRIBE as incentives for this pool, increasing yield, offsetting IL, and giving Synapse governance power in Fei Protocol. IL and convexity risk is further mitigated through vaults having different duration.

Sophisticated options traders and DeFi users can execute this strategy on their own however Ribbon packages this strategy up for investors by using both Hegic and Opyn to find the cheapest on-chain price depending on the size of the trade.

Ribbon Finance works with Opyn to mint oTokens and then subsequently works with market makers (off-chain) to swap oTokens for WETH. This means the Ribbon vault is able to receive the premium in WETH and the market maker receives the premium in oTokens.

The vault sells [Out-The-Money] OTM put options on Opyn on a weekly basis capturing the premium and reinvesting it on a weekly basis to compound yields. If options expire [In-The-Money] ITM then the vault is obligated to buy the underlying asset at the predetermined strike price i.e. ‘buy the dip’. The first Puts Vault product will sell puts against $ETH allowing users to either capture the premium and accrue yield on their $USDC or buy $ETH on dips all automatically through Ribbon. As can be seen in the pay-off diagram below, the maximum profit is pre-defined as the premium received. Selling options are a great strategy to capitalise on theta and volatility decay for those bullish on an asset wanting to buy dips.

Options have a significant role in modern finance and are used by market makers, hedge funds, all the way down to retail traders. Zooming into the retail options trading market, 45% of Robinhood’s Q3 revenue was driven by options trading on their platform.

Selling covered-calls or cash-margined puts have been the most prominent structured product vaults employed in the sector. Covered-calls generate yield for a token by selling call options with a higher strike price than the current token price (out-of-the-money call options). Option buyers pay a premium for the option contract and the premium is directed back to the vault to accrue yield for depositors. Cash-margined puts are similar but in the other direction. Stables are deposited into the vault and used to underwrite put options against a token with a lower strike price than the current value.

So far, structured product vaults have driven the large majority of the adoption of on-chain options. Raw buying and selling of options at various strike prices have just not appealed to crypto users. Structured products abstract away all of the complexities of underwriting options, pricing options, juggling strike prices, and replacing it all with a simple deposit and earn vault.

It’s not just retail users utilizing these structured option vaults either. Protocols are partnering with structured options protocols to do treasury management and to create vaults for its token holders. Utilizing options vaults for yields instead of typical staking vaults removes the need for token emissions to drive yields effectively reducing the overall inflation and sell pressure for the protocol’s tokens.

Robinhood’s success in equity options is driven by retail traders buying and selling options on its platform while the bulk of DeFi adoption has been on simple depositing in options strategy pools. This means DeFi protocols are forced to find buyers (often market makers) off-chain in order to source premium yields. Protocols like Dopex, Lyra, Premia all are built on the foundation of users directly buying and selling options on the protocols.

Options have had a slow start on-chain. Despite options being Robinhood’s top grossing product, retail crypto traders have prefered other forms of leverage like perpetuals. However, there is a rising interest in decentralized options vaults (DOVs). DOVs take user deposits and use the funds to underwrite and subsequently sell the contracts to other parties. In exchange, the buyers pay a premium which is sent back to the DOV as yield for deposits.

The generated yield serves as the revenue of the protocol. Options protocols offering DOVs typically take a cut of the yield generated and may also impose a fee on the total assets deposited.

In terms of revenue efficiency, Options protocols are the second most efficient and generate about four times as much per unit of TVL. While this is significant on a percentage basis, it's important to recognize DOV Options protocols are the second lowest grossing sector mentioned in this report and can only scale revenues relative to the options buying demand.

Futures have no funding curve. The real cost of leverage with futures is the premium you have to incur over current spot price to enter the position. Sometimes, there’s a discount rather than a premium and you essentially have leverage that “pays”. Futures are a good choice for various types of people. Investors with a specific time horizon, options dealers that need to delta/gamma hedge, and people looking to lock in a sell price for their spot assets. The same holds up for perps too.

Squeeth is a DeFi-native derivative that gives exposure to the squared price of ETH. Owning oSQTH has a payoff that increases quadratically as the ETH price increases. It’s a way to make a leveraged bet on ETH, where leverage increases as the price increases, without risking liquidation.

Crab is one of DeFi’s highest returning USDC strategies (+10.09% in just 4 ½ months!). Jumbo Crab allows users to receive lower price impact by matching large deposits with large withdrawals or conducting an auction.

The strategy focuses on ETH accumulation. DeFi’s open ecosystem of programmable “money legos” makes this possible in a crypto-native way. It combines Crab with a lending protocol to earn additional ETH returns when Squeeth volatility is lower than expected.

You may have read one of the many articles describing how squeeth can be used to hedgeoptions or a Uniswap v3 LP position. In this article, I describe how to do the opposite: how to use Uniswap v3 to perfectly hedge a squeeth, options, or any positive convexity instrument over an arbitrary range.

II.4 Panoptic ERC1155 composite option token. Panoptic will allow users to sell undercollateralized options as a core element of the protocol (section IV). This is in contrast to all other on-chain option protocols (except Opyn v2), which always require all positions to be 100% backed by collateral. Panoptic will allow the creation of undercollateralized options by using margin account collateral requirements similar to those developed by traditional financial institutions.

This is the primary difference between selling an option on Uniswap V3 vs. selling an option on a platform like Opyn. Rather than receiving your premium upfront (when the position is opened), you receive the premium when the price crosses above/below your position. This can also be thought of as your option being “exercised”.

Squeeth almost perfectly hedges Uni v3 LP positions. Providing liquidity on Uniswap is short gamma, since large moves in either direction disproportionately hurt you: more broadly, the nature of LP’ing is a gamble that the trading fees received outweigh the fact that you are selling volatility i.e. that large moves will not occur. Amongst its other applications, Squeeth hedges IL through acting as long gamma, and has other desirable properties such as its lack of rollover. It is a rather novel primitive, and the Opyn team should be commended for its development.

Opyn has been used as settlement layer for Ribbon, StakeDAO, and others during a long time. For that reason, using TVL as metric, Opyn would be the best order book, even though there’s no liquidity in the order book per se. All options minted are settled on auctions off-chain.

One notable difference is the presence or absence of fees. The majority of order books, like Opyn and Zeta, are "feeless" and do not charge any fees for their services. Others, like Opium Finance, have a fixed fee structure with a 5% minting fee and a 0.1% settlement fee.

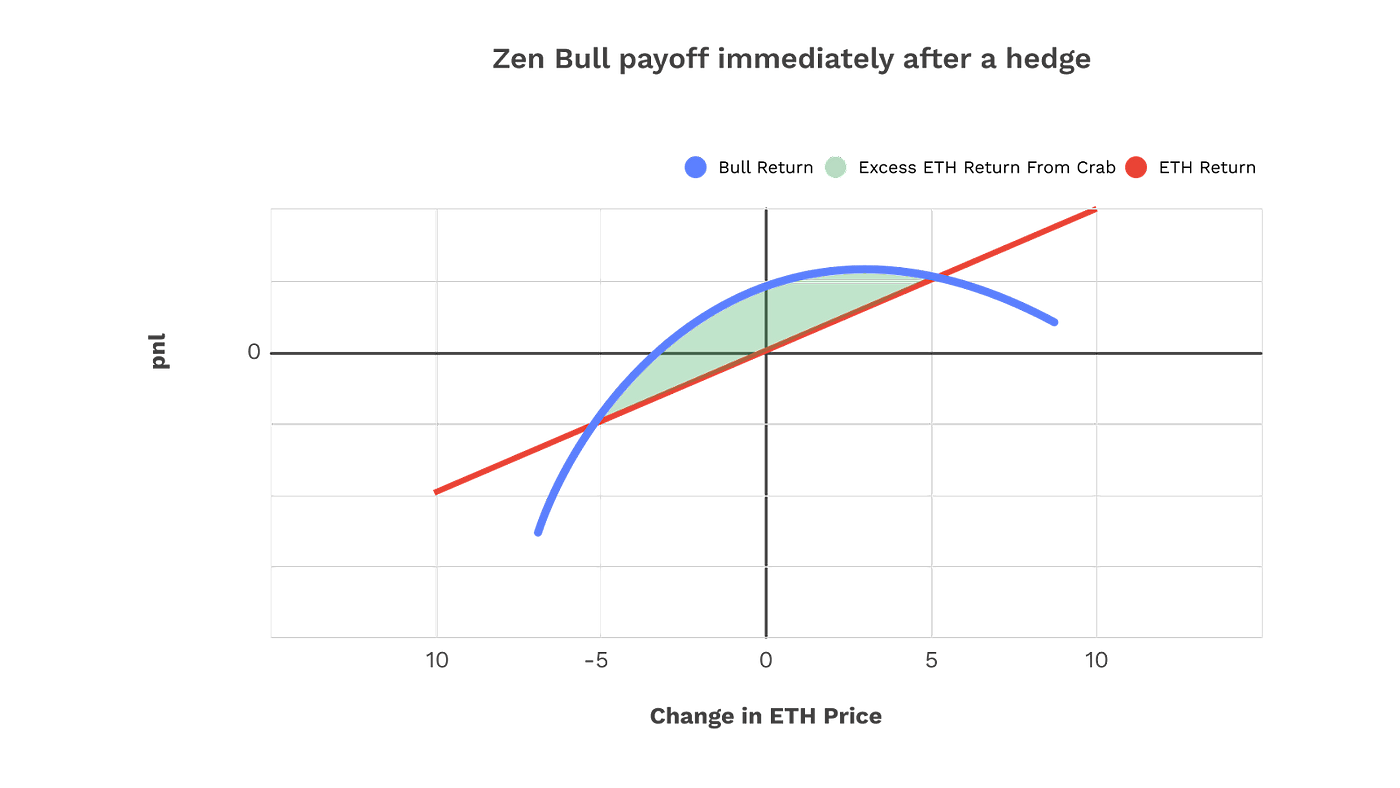

The contracts we have audited pertain to the Bull Strategy, which aims to maintain 100% exposure to ETH (i.e. delta of one) while profiting from the premiums generated by the Crab Strategy. This is achieved by combining a position in Crab with a leveraged position on Euler, where WETH is used as collateral and USDC is borrowed and sold in order to create the leverage. Since the Crab Strategy is delta neutral, the positive exposure to ETH is given by the leveraged position on Euler.

If we choose the volatility σ of a crypto asset like Ether to be between 100% to 150% per year (using data from Genesis Volatility or the Opyn options analytics page) and a drift term μ of less than 1% per year, then most of the numbers in the expression above will be somewhat small compared to 1 for short time intervals (for instance μ-σ²/2 = 0.008 in that case).

Deridex and Opyn are charged with failing to register as a swap execution facility (SEF) or designated contract market (DCM), failing to register as a futures commission merchant (FCM), and failing to adopt a customer identification program as part of a Bank Secrecy Act compliance program, as required of FCMs. ZeroEx, Opyn and Deridex are also charged with illegally offering leveraged and margined retail commodity transactions in digital assets.

Each respondent engaged in these activities in connection with blockchain-based software protocols and smart contracts, commonly referred to as DeFi, that functioned similarly to trading platforms, and which purported to offer users the ability to engage in transactions in a decentralized environment. The orders require that Opyn, ZeroEx, and Deridex pay civil monetary penalties of $250,000, $200,000, and $100,000, respectively, and cease and desist from violating the Commodity Exchange Act (CEA) and CFTC regulations, as charged.